AMD vs. Nvidia AI: Helios and the Coming Fight

AMD's Helios: A Rack-Scale Gamble That Might Just Pay Off

AMD is stepping into the AI infrastructure ring with its Helios rack-scale system, slated for a 2026 release. The ambition is clear: take on Nvidia's dominance in the AI datacenter, head-on. But ambition alone doesn't move markets. Let's dig into the numbers and see if this has a shot.

AMD's Q3 2025 financials paint a promising picture. Server CPU revenue hit an all-time high, fueled by the adoption of their 5th Gen Epyc Turin processors. Dr. Lisa Su, during the investor call, highlighted that these new processors accounted for nearly half of Epyc revenue. That’s a significant shift in product mix (and, presumably, ASP – average selling price). But, as always, the devil is in the details. What constituted "nearly half?" 49%? 45%? The difference is substantial when you're talking about billions of dollars.

Helios: A Direct Shot at Nvidia

Helios, as AMD presented it, is a direct competitor to Nvidia's DGX GB200 NVL72. The idea is to treat a rack full of accelerators as a single, massive GPU. Su emphasized that Helios integrates Instinct MI400 Series GPUs, Epyc Venice CPUs, and Pensando NICs. The ZT Systems team (acquired last year) is playing a key role in development. (The acquisition cost was substantial – reported at $2.1 billion).

Crucially, AMD is targeting Meta's new open rack wide standard. This is smart. Aligning with an industry standard makes adoption easier, especially for hyperscalers who hate vendor lock-in. But, standards are also a double-edged sword. They can commoditize the market, squeezing margins.

The MI400 series GPUs and Venice CPUs (6th-gen Epyc, built on TSMC's 2nm process) are both critical pieces of this puzzle. Production on TSMC's bleeding edge is expensive, and any delays could derail the entire Helios timeline. AMD taking AI fight to Nvidia with Helios rack-scale system.

AMD is also seeing increased CPU demand, driven by AI workloads. As Su noted, "AI is requiring quite a bit of general-purpose compute." This is a key point often missed in the GPU-centric hype. AI isn't just about GPUs; it needs CPUs for data preprocessing, model orchestration, and a host of other tasks. So, while everyone is focused on the GPU battle, AMD could quietly win ground on the CPU side.

However, AMD's CFO, Jean Hu, was cagey about the financial impact of Helios in 2026. "We're not guiding 2026, but our priority in datacenter GPU business is to really expand the top line revenue growth and the gross margin dollars." Translation: They're not promising immediate returns. This isn't surprising. Rack-scale systems are complex, and adoption cycles are long. It takes time to design, test, and deploy these solutions at scale.

The OpenAI Question

UBS analyst Timothy Arcuri raised a crucial point about AMD's agreement with OpenAI. He suggested that OpenAI could represent "something like half of your datacenter GPU revenue in the 2027, 2028 time frame." That's a massive concentration risk. While Su brushed it aside, stating that AMD is dimensioning the supply chain to support multiple large customers, the question remains: What happens if OpenAI shifts its strategy or develops its own silicon?

I've looked at hundreds of these filings, and this particular analyst's question is unusually direct. It suggests that the market, at least, is concerned about AMD's reliance on a single, albeit large, customer.

Looking at AMD's overall financials, revenue grew about 36%—to be more exact, 36.1%—to $9.2 billion in Q3 2025. The datacenter business was up 22% to $4.3 billion. Client and gaming systems jumped 73% to $4 billion. The embedded portfolio declined 8% year-on-year to $857 million. This decline is a bit of a red flag. The embedded market is typically more stable than client or gaming, so an 8% drop suggests some underlying weakness. Is it cyclical? Is it competition? The report doesn't say, and that's a problem.

AMD forecasts Q4 2025 revenue of $9.6 billion (plus or minus $300 million), representing roughly 25% year-on-year growth. Notably, this outlook excludes any revenue from MI308 shipments to China. This is another risk factor. Geopolitical tensions could disrupt supply chains and limit AMD's access to a critical market.

A Calculated Bet, Not a Sure Thing

AMD's Helios is a bold move, but it's not a guaranteed victory. The company faces significant challenges, including competition from Nvidia, execution risks in bringing new products to market, and geopolitical uncertainties. The success of Helios hinges on AMD's ability to deliver on its promises and navigate a rapidly changing market. The numbers suggest potential, but potential doesn't pay the bills.

Is AMD Overplaying Its Hand?

-

Warren Buffett's OXY Stock Play: The Latest Drama, Buffett's Angle, and Why You Shouldn't Believe the Hype

Solet'sgetthisstraight.Occide...

-

The Business of Plasma Donation: How the Process Works and Who the Key Players Are

Theterm"plasma"suffersfromas...

-

The Great Up-Leveling: What's Happening Now and How We Step Up

Haveyoueverfeltlikeyou'redri...

-

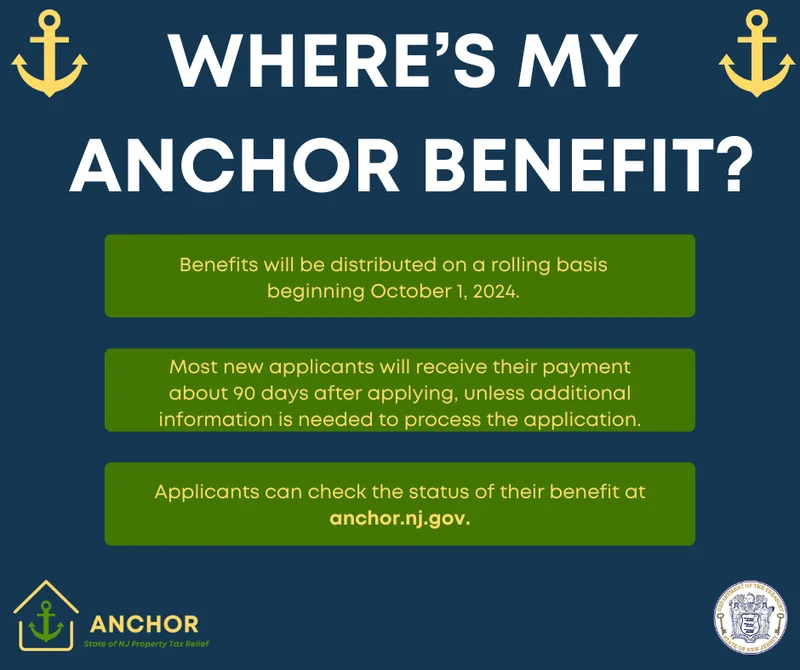

NJ's ANCHOR Program: A Blueprint for Tax Relief, Your 2024 Payment, and What Comes Next

NewJersey'sANCHORProgramIsn't...

-

The Future of Auto Parts: How to Find Any Part Instantly and What Comes Next

Walkintoany`autoparts`store—a...

- Search

- Recently Published

-

- Stock Market 'News': Today's US Market Spin and the 'Live' Updates

- IRS Direct Deposit Relief Payments: What This Breakthrough Means for Your Financial Prosperity

- Bilbao: What the Data Reveals

- Outback Steakhouse Closures: The Financials Behind the Shutdown and Which Locations Are Gone

- The Burger Bubble Just Popped: Why Your Go-To Spot is Next on the Chopping Block

- The Bio-Hacked Human: What the New Science of the Core Reveals About Our Future

- Ore: What It Is and Why It Matters

- Firo: What is it?

- Avelo Airlines: FAA Cuts and the Lakeland Linder Opportunity

- Rocket Launch Today: What Happened and the Mystery Fireball

- Tag list

-

- Blockchain (11)

- Decentralization (5)

- Smart Contracts (4)

- Cryptocurrency (26)

- DeFi (5)

- Bitcoin (29)

- Trump (5)

- Ethereum (8)

- Pudgy Penguins (5)

- NFT (5)

- Solana (5)

- cryptocurrency (6)

- XRP (3)

- Airdrop (3)

- MicroStrategy (3)

- Stablecoin (3)

- Digital Assets (3)

- PENGU (3)

- Plasma (5)

- Zcash (6)

- Aster (4)

- investment advisor (4)

- crypto exchange binance (3)

- bitcoin price (3)

- SX Network (3)