Stock Market 'News': Today's US Market Spin and the 'Live' Updates

The market on Friday, November 14, 2025, felt less like a decisive close to the trading week and more like a collective shrug. The Nasdaq Composite managed a thin 0.13% gain, snapping a three-day losing streak to finish at 22,900.59. Nasdaq closes higher, snapping three-day losing streak as tech stocks recover some ground - CNBC But don’t let that fool you into thinking the us stock market found its footing. The S&P 500 dipped 0.05% to 6,734.11, and the Dow Jones Industrial Average shed 309.74 points (a 0.65% loss), settling at 47,147.48. This isn't exactly a roaring comeback after Thursday's brutal session, which saw major U.S. indexes post their worst one-day performance since October 10—the Dow alone dropped about 800 points that day. The week as a whole remained a mixed bag, with the Nasdaq down 0.5%, while the S&P 500 eked out a 0.1% gain and the Dow a slightly better 0.3%. What we’re witnessing isn't a clear direction; it's a market struggling to reconcile conflicting narratives, primarily the enduring promise of AI against a growing undertow of economic realism.

The AI Paradox: When Data Points Collide

The immediate story from Friday's stock market today news was the rebound in tech stocks. Nvidia, Oracle, Palantir Technologies, and Tesla all reversed course after significant losses, pushing the Technology Select Sector SPDR Fund (XLK) up 0.5%. This looks good on the surface, a testament to the "risk-on" appetite some investors still carry. But dig a little deeper, and the picture gets murky. My analysis suggests this isn't a broad-based tech surge, but a concentrated bet. Rebecca Homkes, an economist, nailed it: the stock market today is "a giant bet on AI right now," with just 10 companies driving most of the gains.

The concern here isn't just about valuation, though that's a huge piece of the puzzle. David Krakauer of Mercer Advisors correctly pointed out that AI is "truly testing the limits of Wall Street spreadsheets." When valuations are this stretched, small movements in expectations have outsized effects. Take Oracle, for example. Its growth is particularly reliant on a cloud deal with OpenAI, and it simply doesn’t have the same cash reserves as the hyperscalers. This makes its position inherently more precarious. The recent wipeout in Oracle shares, preceding Friday's tepid rebound, spooked investors precisely because it highlighted the fragility of elevated tech valuations, the massive debt financing often underpinning these plays, and the soaring capital expenditure plans required for AI infrastructure.

This brings me to a personal observation: I've looked at hundreds of these market structures over my career, and the current concentration around a handful of AI titans feels particularly precarious. It’s like watching a tightrope walker carry an increasingly heavy load across the Grand Canyon. You admire the skill, but the inherent risk grows with every step, and the margin for error shrinks to nothing. Can a market so heavily reliant on a few players truly be robust? And how much of this "AI revolution" is quantifiable productivity, and how much is merely a narrative-driven valuation game? These are the questions that keep me up, far more than the daily ticks of the Dow.

The Fed's Shadow and a Fractured Reality

Beyond the ai news and tech drama, a much more fundamental shift is underway, one that could pull the rug out from under even the most optimistic projections. Traders are now pricing in less than a 50% chance of a Federal Reserve quarter-percentage-point rate cut in December. Let me be more exact: that's a significant drop from 62.9% earlier this week, and a truly staggering plunge from 95.5% just a month ago. This isn't a minor adjustment; it's a complete recalibration of expectations. Investors were, to put it mildly, "counting on a December rate cut to revive the economy and risk-taking on Wall Street." Kansas City Federal Reserve President Jeffrey Schmid didn't help matters, reiterating his opposition to further interest rate cuts on Friday, citing sticky inflation.

This reality check from the Fed is creating a deeply fractured market. On one hand, eight S&P 500 stocks, including Assurant and Hartford Financial, hit new all-time highs on Friday. On the other, eight different S&P 500 stocks—think Charter Communications and Molina Healthcare—plunged to new 52-week lows on the very same day. This isn't the sign of a healthy, uniformly growing economy. It's a market where a few specific narratives are driving extreme outcomes, while others are being left in the dust. The consumer discretionary sector, for instance, was the worst-performing S&P 500 sector this week, slipping over 2% and on track for its biggest monthly loss for November. When consumers pull back, it's usually a red flag.

And then there's the crypto market, often seen as a bellwether for speculative risk-taking. Bitcoin (or btc as some call it) dipped below $95,000 on Friday, continuing a four-day decline and trading at $96,293, down 3.5% on the day. Even more telling, Strategy stock—a bitcoin treasury stock—plunged over 17% this week, heading for its worst week in a year and trading near its 52-week low of $194.56. This is a clear "risk-off" signal, a stark contrast to the tech rebound. While the US government shutdown (the longest in history, ending Wednesday evening after more than six weeks) is now resolved, its lingering effects and the ongoing geopolitical tensions (Iran seizing an oil tanker, Russia halting oil exports due to Ukrainian strikes, pushing crude oil over $60 a barrel) only add layers of uncertainty to an already complex equation. The market, it seems, is trying to dance in two different directions at once.

The Great AI Divide: A Valuation Mirage?

The comparisons to the dot-com era are inevitable, and frankly, warranted. The startling run-up in AI-related stocks is prompting questions, and rightly so. Should you worry about an AI bubble? Investment pros weigh in. - CBS News Goldman Sachs analysts note that current valuations for the "Magnificent 7" (Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, Tesla) are "roughly half" the median price-to-earnings ratio of the largest seven companies during the late 1990s dot-com bubble. Federal Reserve Chair Jerome Powell has also weighed in, stating that current highly valued companies like those in AI have "actual earnings," unlike many "ideas rather than companies" during the dot-com period. Nvidia's revenue, for instance, more than doubled to $130 billion in its last fiscal year, with profit surging 145%. These are undeniably strong fundamentals.

However, a methodological critique is in order here. While the P/E ratios might be "half," the sheer scale and market concentration are unprecedented. The Magnificent 7 collectively represent a record 37% of the S&P 500's total market capitalization. That's an enormous weighting. And while they have earnings, economists are still questioning whether AI will be as transformative for businesses as proponents claim, and if the trillions in capital spending on AI infrastructure will truly pay off through a sustained productivity boom. It's one thing to have earnings; it's another to justify valuations that bake in a future of exponential, unprecedented growth. When you're dealing with such an outsized proportion of the market, any tremor in these giants sends shockwaves everywhere. We're not just betting on the future; we're betting the entire farm on a handful of very specific, very expensive horses.

The Illusion of Stability

The market is currently a complex tapestry of conflicting data points, with threads of AI optimism woven through a backdrop of rising interest rate anxiety and underlying economic fragility. The rebound in tech on Friday, while welcome for some portfolios, looks more like a brief breath-holding moment than a true change in trajectory. The plummeting expectations for a December rate cut, coupled with the stark divergence between market winners and losers, paints a picture of profound uncertainty. The geopolitical chessboard and the lingering questions about AI's true economic impact only add to the fog. Investors are repositioning, yes, but into what exactly? The "risk-on" and "risk-off" patterns suggest a market that doesn't know whether to lean forward or brace for impact. Can we really sustain these AI-driven valuations if the cost of capital remains high and the broader economy struggles? The data, as I see it, is screaming caution.

-

Warren Buffett's OXY Stock Play: The Latest Drama, Buffett's Angle, and Why You Shouldn't Believe the Hype

Solet'sgetthisstraight.Occide...

-

The Business of Plasma Donation: How the Process Works and Who the Key Players Are

Theterm"plasma"suffersfromas...

-

The Great Up-Leveling: What's Happening Now and How We Step Up

Haveyoueverfeltlikeyou'redri...

-

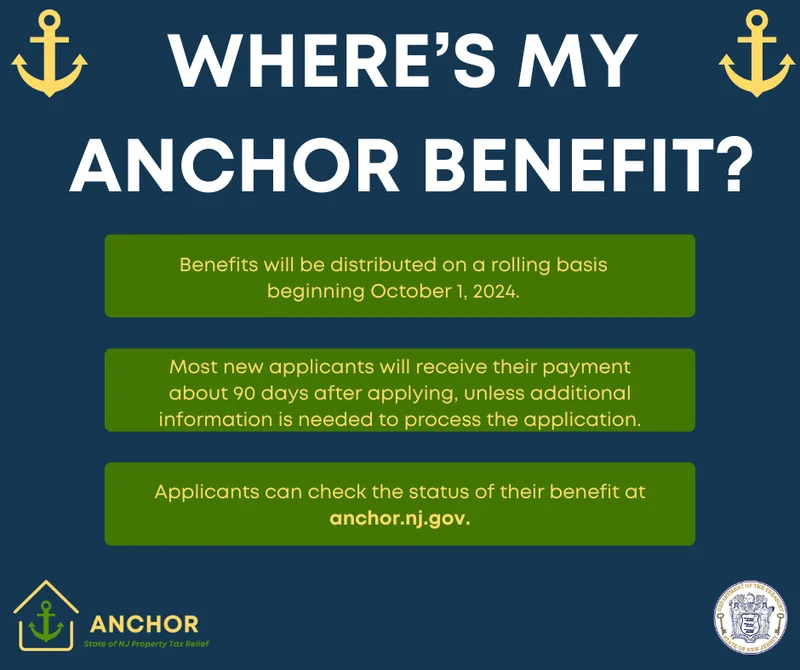

NJ's ANCHOR Program: A Blueprint for Tax Relief, Your 2024 Payment, and What Comes Next

NewJersey'sANCHORProgramIsn't...

-

The Future of Auto Parts: How to Find Any Part Instantly and What Comes Next

Walkintoany`autoparts`store—a...

- Search

- Recently Published

-

- Stock Market 'News': Today's US Market Spin and the 'Live' Updates

- IRS Direct Deposit Relief Payments: What This Breakthrough Means for Your Financial Prosperity

- Bilbao: What the Data Reveals

- Outback Steakhouse Closures: The Financials Behind the Shutdown and Which Locations Are Gone

- The Burger Bubble Just Popped: Why Your Go-To Spot is Next on the Chopping Block

- The Bio-Hacked Human: What the New Science of the Core Reveals About Our Future

- Ore: What It Is and Why It Matters

- Firo: What is it?

- Avelo Airlines: FAA Cuts and the Lakeland Linder Opportunity

- Rocket Launch Today: What Happened and the Mystery Fireball

- Tag list

-

- Blockchain (11)

- Decentralization (5)

- Smart Contracts (4)

- Cryptocurrency (26)

- DeFi (5)

- Bitcoin (29)

- Trump (5)

- Ethereum (8)

- Pudgy Penguins (5)

- NFT (5)

- Solana (5)

- cryptocurrency (6)

- XRP (3)

- Airdrop (3)

- MicroStrategy (3)

- Stablecoin (3)

- Digital Assets (3)

- PENGU (3)

- Plasma (5)

- Zcash (6)

- Aster (4)

- investment advisor (4)

- crypto exchange binance (3)

- bitcoin price (3)

- SX Network (3)